Topic: beginner’s guide to trading and investing

It’s easy, but you still have to do the work rather than waste time on social media

The most important thing is to not stray outside your circle of competence; do what’s easy for you, what’s compatible with your level of effort and dedicated time.

Start carefully, don’t rush, don’t use leverage, don’t short, keep notes, admit to and learn from your mistakes

Then it’s easy.

Length: perhaps a little on the long side, 15-30 minutes

Interview with a blood sucking vampire squid

I was recently interviewed (together with Ludvig at SGM) on the basics of trading, investing and health.

Some of my answers were met with disbelief and denial. That inspired me to write a short summary of the interview and elaborate a bit on my answers and thoughts about investing.

Note of caution: be prepared for contradictions such as “buy and hold, but use stop losses… and double up on falling shares“, “track just one important value driver, but never trust just one indicator“, “never trade on tips, but listen to the information content in them“. As with everything interesting, the answer is not binary, but a superpositioned state along the entire spectrum.

Investing is easy

On the one hand I said investing is easy (anything works, literally)

On the other I said you have to believe you are better than average if you are aiming for being an active investor or trader. I clarified the latter by stating it meant being better than thousands upon thousands of other interested, intelligent and hard working private and professional investors with access to sophisticated tools and research.

In a way, I can understand how those two statements seem contradictory. However, they aren’t.

When I claim it is easy, I mean that if you consistently spend, e.g., half an hour a day or 4 hours a week (Tim Ferriss style…) on focused study, “deliberate practice” (Anders Ericsson), of the fundamentals of a particular stock, index, instrument or other financial phenomena, you probably will become good enough to make decent returns sooner or later. With “a”, I really mean just “one”.

How did

Dr Strange

become such a good surgeon?

-Years of deliberate practice.

There’s just a small catch; you actually have to do it, rather than spend those four hours mudslinging on social media forums.

The most important thing

Some of the most important things you need to know are:

You are biased in numerous ways (1, 2, 3, 4, 5). Counter that by keeping thorough notes of your profits and losses, of your reasons, decisions and outcomes.

- Investing Psychology, Tim Richards

- All I Want To Know…, Peter Bevelin

- The Most Important Thing, Howard Marks

- Predictably Irrational, Dan Ariely

- Thinking Fast And Slow, Daniel Kahneman

No social media. It is very difficult to extract any valuable information from social media forums. Whatever time you are currently spending touting and defending your own investments, or arguing with strangers over things neither of you actually know anything about; invest that time reading books and annual reports instead.

Listen to your “adversaries”; try to see the other side. They are usually neither stupid nor evil. More likely they (or you) are just misinformed or not seeing the whole picture. Try to understand exactly why they think your undervalued stock is overvalued. Write down what it would take for you to change your mind. Could that ever happen?

Are short sellers* stupid,

evil

or both?

*of your favorite stock

The biggest mistake is not admitting your mistakes and taking corrective action in time.

You are going to make a lot of mistakes. Some of them will be of your own making due to carelessness (“I’m on a roll”), a sense of urgency (never trade in amygdala mode, i.e. when trapped in the strong fight/flight/love feelings of your so called reptile brain), too little knowledge or believing your own Excel spreadsheet forecasts. Some mistakes will be turning a blind eye to changing fundamentals for too long.

Hope is not a strategy

So, since you are only human (Thinking Fast And Slow*, Predictably Irrational*) and since the future is unpredictable (The Black Swan*) you will make a lot of errors. That’s fine as long as you are being honest and objective about it. Never “cross your fingers” (1), rationalize (“margins could be a little higher in the future”) or moralize (“central bankers are evil, they shouldn’t…”) in order to defend a losing position.

*see my book recommendations here, and specifically my investing recommendations here

- Hope is not a strategy

- Nobody cares what price you bought at and neither should you. You should always evaluate your position with total equanimity, not hope for a magical return to your break-even price.

- Take your stop loss as soon as the fundamentals tell you too

- Don’t try to make up for your losses in the same stock, or by increasing the risk

On catching knives. If you are not ready to double up on a falling stock (given unchanging fundamentals), you probably should never have bought it to begin with (your analysis was wrong or sloppy), and consequently you should get out altogether sooner rather than later.

- Don’t just initiate stop-loss procedures for the sake of it (unless it’s part of a time-tested strategy)

- Buy a little (more) on the first sharp drop. Buy a lot more if it falls by a lot after that. Again, given fundamentals remain intact (see how I did it in Opus here)

You need to be patient

- Patient when commencing your studies

- Patient when scaling up your operations, learning from experience, realizing where your strengths and weaknesses are, getting to know your biases, before increasing your risk taking

- Patient when waiting for opportunities

- Patient when waiting for the effects of compound interest. Rushing profits often leads to losses. If you feel hurried, don’t trade.

Should you invest in stocks at all?

Actually before even considering investing or trading in stocks or similar instrument, you should first ask yourself the following questions:

- Will I put in the required amount of time and effort?

- Could I be better off by investing in, e.g., cash (the most hated asset class right now), bonds, education or a business of my own instead?

Remember that the current New TINA* Paradigm meme is all wrong

*TINA=There Is No Alternative (to stocks)

The unbearable lightness of investing:

It is easy.

However it’s just as easy to trick yourself into thinking it’s even easier.

- Confidence. The less you know about a topic the more confident you are likely to be

- Authorities. In particular in areas of great uncertainty (such as in the case of the random walk of stock markets) it’s easy to fall prey to camouflaged charlatans; false authorities giving away stock tips. Several experiments show certain cognitive and questioning parts of the brain are less active when receiving orders or suggestions from a perceived authority (which in the case of stocks is anybody talking confidently or exhibiting an impressive track record).

- Availability bias: it’s all too easy to simply analyse whatever stock or piece of information that happens to fall into your lap, instead of systematically screen a certain “universe” of stocks and then systematically look for the most important value drivers and analyze those.

- For example, you do not know or understand Apple just because you own an iPhone, or WalMart because you shop there. Burning batteries in Samsung phones may or may not be relevant for Apple’s share price, but be sure to check in what way and to what extent. What if Apple is using a similar design or battery supplier? What if Android users will only look for other Android replacement phones?

Don’t over-analyze. Spend a reasonable amount of time on the most important value drivers and then track them. Spend much more time on finding out which drivers are the more important ones, than trying to track dozens of more or less relevant data series.

Actually you could begin with tracking and investing based on only one single driver, such as the number of iPhones sold, their gross margin or, e.g., H&M’s number of new stores. I’m not saying it works, but it’s a start.

Don’t believe the hype

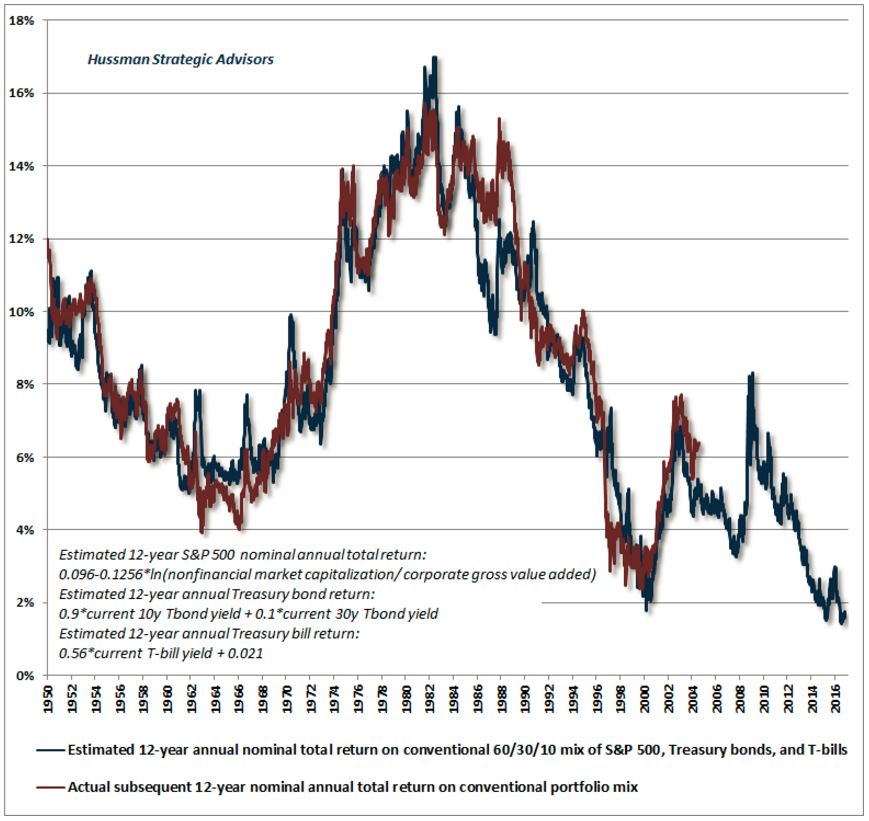

No holy grail investing. There is no one magic macro indicator that will tell you whether we are in a bull or a bear market. No matter if you find correlations between total stock market returns and, e.g., NYSE margin debt, the Fed model spread, the yield curve or the Shiller P/E, you just shouldn’t believe it will hold in the future or reliably provide a timely signal when to go all in on buying or selling the market. The same logic usually applies to single stocks as well.

The chart below, however, is one of the indicators I think you should keep in your tool box.

Never trade on tips – it’s one of the most stupid things you can ever do in investing or trading (this piece of advice seemed to be perhaps the most contentious one during the interview). The reason you shouldn’t is that you don’t know who the tipster is, what his agenda is, how well founded his reasons are etc. And even if you do, you can never count on getting the sell tip in a timely matter in the future.

Do the math yourself instead. See for yourself, both when to buy and when to sell. Genji Gambashi. You could of course use a tip as a starting point for your own research, but then you wouldn’t be trading on the tip.

Never trade on momentum – for much the same reasons as the anti-tip tip above (I mean, if the trade turns sour, what do you do? When? Why did you actually buy to begin with?)

Well, that is unless you are already an active, experienced and competent day trading professional that know what you are doing and are good at stopping your losses. But if you are, what the f* are you doing here, reading this article? :p

Don’t buy what you can’t afford to lose (If I got a comeback on that one?: “but then you would never dare buy anything“).

The thing is you will lose sometimes; Just since the year 2000, the stock markets have halved at two different occasions (for short, 2002 and 2008), and it’s not unlikely they will soon again (all relevant variables are at the same or worse levels than they were right before those two downturns, not to mention a few others during the last century).

It’s better to understand this before it happens than after the fact. Remember though, that there is a difference between what you definitely can’t afford to lose and what you’d just rather not lose but actually could and are willing to bet.

Don’t use leverage and don’t short the market. In the context of not betting what you can’t lose, I’d like to caution against borrowing to invest or speculate. Speculating with borrowed money implies you are in a rush to make money (bad idea in itself), and could lead to forced selling just when you actually should buy more.

I’d also like to point out that shorting stocks or the entire market is very difficult and should be limited to between 0 and 10 percent of the time (some should never attempt it), and only if you are very experienced, know exactly what you are doing and can afford to be wrong.

Investing is a piece of cake

-if you’re systematic and humble:

- Investing is easy (kind of… however, if you think it is you might want to think again), if you put in the adequate amount of work for your investment strategy

- Certain hedge funds and index funds require less work than, e.g., some investment companies.

- At the top of the pyramid you’ll find individual stocks where you’ll compete with thousands if not millions of smart and ambitious people. Do you actually know or understand something they don’t? If not, study more or go back to level A.

- Yes, you need to know more than others, work harder than others, or consistently have more luck than others (sic), if you want to make bigger returns than others. And, no, high risk does emphatically not guarantee higher returns. It wouldn’t be called “risk” then, would it?

- This might be a bit over the top for most… but my post here still could serve as inspiration for the aspiring value investor

- Take a complete break from investing for a week or a month every now and then, i.e. close all your positions and start from the beginning. You were probably on the sidelines for decades anyway when you were a kid.

- Be systematic and humble. If you aren’t humble and ready to learn and abide by several unwritten rules (this article lists a few), you are probably better off being a passive investor: buy whatever will make you sleep well and never look at your investments, until you want to use them for a large purchase or your retirement

- Daily exercise is very good for your investment successes. It makes you smarter, more creative, happier and less stressed, not to mention able to keep at the game for decades longer

- Take a walk whenever feeling stressed or about to take a decision based on emotions rather than facts and cold reasoning. Just getting out of the box relieves stress, clears the brain and prevents you physically from making passion trades (a big no-no). Walking new paths stimulates new thoughts as well as the general ability and willingness to break out of homeostasis.

- Walk briskly for half an hour every day (take a de-tour on the way home, get off a few stops early and walk the rest of the way, buy your lunch further away from the office…). It counters aging and promotes growth in the thinking parts of your brain (pre frontal cortex), not to mention stimulates creativity and happiness in the moment

- For the advanced walker, make small 10-second spurts every now and then. If it feels uncomfortable, not least in a suit, save that for the gym or track later

- Additional resources from my archive

- Gold

- My quattro stagione investment strategy

- Top ten investment mistakes (consistently avoiding stupid mistakes is much more important in investing than hitting homeruns)

Summary – do a little with excellence

-not a lot poorly

Investing can be easy, if you just avoid the worst mistakes instead of looking to hitchhike with rockets taking off:

- Be patient; do the work, don’t bet the farm, don’t borrow, don’t short

- Do only what you can and have time for – take breaks when needed

- Study, not argue; truly listen to the other side (Ender’s Game)

- Readily admit and remedy mistakes. Losses are just lessons (Dao of Capital)

- Keep notes of your decisions, your mistakes, your best practices; and consult them before investing (Commonplacing with Evernote)

- Trust no one but yourself, be independent – neither contrarian nor wall street meat (a pretty good book). Never trade on tips.

- Stay humble

- DON’T PANIC

Do you want more free and valuable stuff?

Join tens of thousands on my site, and sign up for my free newsletter. There is a free investment lessons e-book waiting for you.

Are you curious, philosophical, and looking for truth, understanding and happiness? Do you know more people like you and me? Please help me spread my insights about how to live a happy, healthy and wealthy life in modern society – tell others about this site, share it in your social networks.

Limited. Every now and then I clean my e-mailing list from inactive subscribers, to make room for new ones. Sooner or later I might introduce some kind of a latecomer fee to finance the growing list. However, it will always be free for incumbent, active subscribers.

Mistakes are the foundation of my knowledge, not least in my private investments since I retired from professional investing.

Share. I sincerely hope they can be of use to you and others; so please share this article and my site with your social networks.